Quick Answer

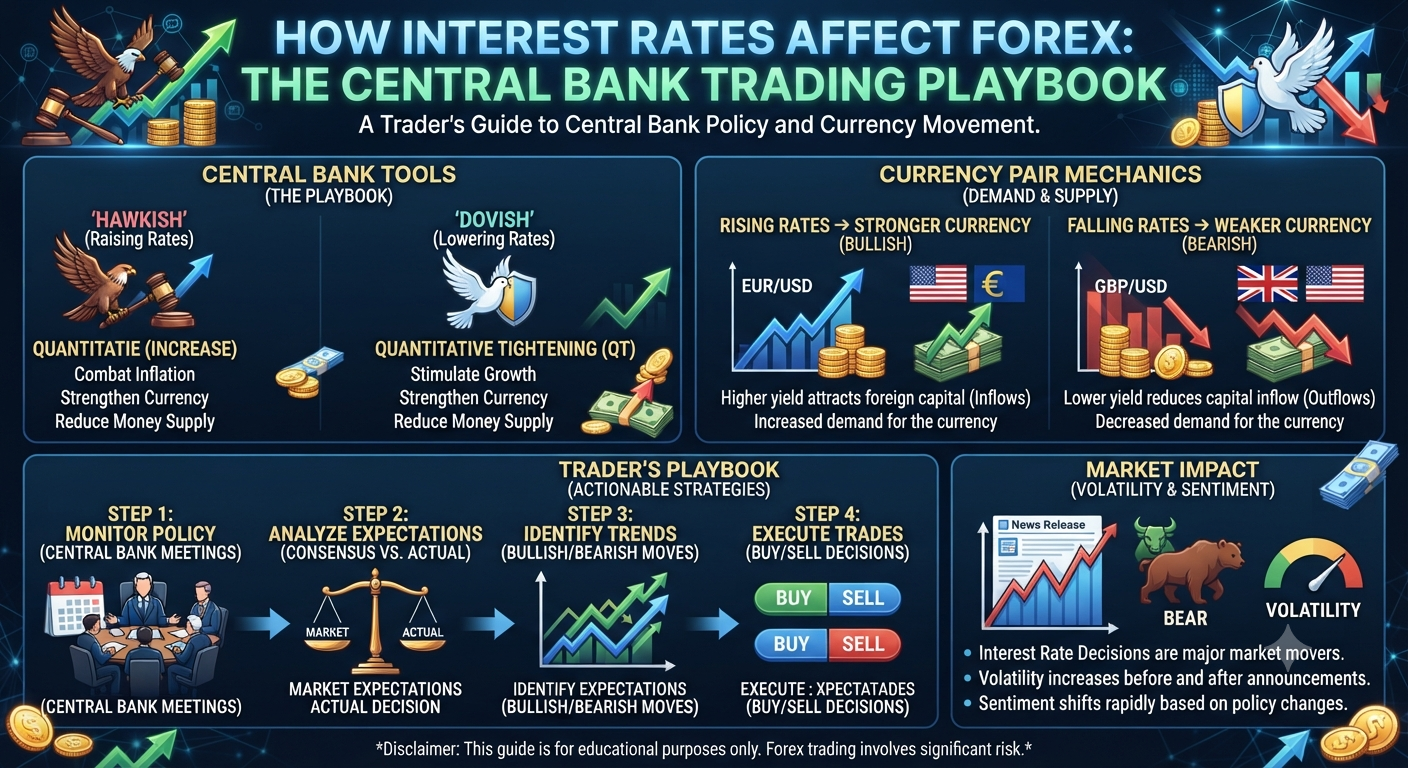

Interest rate decisions by central banks are the single most powerful fundamental driver of currency values in the forex market. When a central bank raises interest rates, its currency typically strengthens because higher rates attract foreign capital seeking greater yield on deposits and government bonds, increasing demand for that currency. When rates are cut, the currency typically weakens as yield differentials become less favorable. In 2026, understanding the interest rate policies of the Federal Reserve, European Central Bank, Bank of England, and Bank of Japan and how their divergence or convergence creates directional forex opportunities is the foundation of professional fundamental analysis.

Why Interest Rate Decisions Are the Most Powerful Forex Driver

- Quick Answer

- Why Interest Rate Decisions Are the Most Powerful Forex Driver

- How to Trade Fed Rate Decisions: The Before and After Strategy

- Interest Rate Differentials and the Carry Trade Strategy Explained

- ECB, BOE, BOJ, and RBA: How Each Central Bank Moves Its Currency in 2026

- Building a Macro Fundamental Bias for Directional Forex Trading

- Key Takeaways on Interest Rates and Forex in 2026

The connection between interest rates and currency values operates through a mechanism called the interest rate differential. When two countries have different interest rates, capital naturally flows toward the country offering higher returns. This flow creates demand for the higher-yielding currency, which pushes its value higher against the lower-yielding currency.

Consider a simplified example from 2026 conditions. If the Federal Reserve maintains a benchmark interest rate of 4.25% while the Bank of Japan holds its policy rate at 0.50%, a US Treasury bond yields approximately 3.75 percentage points more per year than a comparable Japanese government bond. International investors, seeking to maximize return on their bond holdings, convert yen into dollars to purchase US Treasuries, creating sustained demand for USD and selling pressure on JPY. This capital flow dynamic is the primary structural reason USD/JPY has remained elevated throughout 2025 and into 2026 despite occasional BOJ policy adjustments.

This mechanism operates at the institutional level across trillions of dollars of global capital allocation decisions. Sovereign wealth funds, pension funds, insurance companies, and asset managers continuously rebalance bond portfolios toward the highest-yielding safe assets, and these rebalancing flows dwarf the daily speculative trading volume in any single forex pair. Understanding this structural capital flow dynamic is what allows fundamental analysis to provide multi-week and multi-month directional context for forex positions.

The relationship between interest rates and currencies is not instantaneous or perfectly linear. Markets are forward-looking, meaning they price in expected future rate decisions long before they occur. By the time an actual rate change is announced, significant portions of its currency impact may already be priced in from weeks of forward guidance, economic data releases, and central bank communication. This is the origin of the market maxim "buy the rumor, sell the fact": a currency may actually weaken after an expected rate hike is announced because all buyers who expected the hike have already bought, and there are no remaining buyers to continue pushing the currency higher.

How to Trade Fed Rate Decisions: The Before and After Strategy

The Federal Reserve's Federal Open Market Committee (FOMC) meets eight times per year. In 2026, under a measured rate-cutting cycle that began in late 2023, FOMC meetings have continued to generate significant forex market volatility because each meeting brings potential updates to the pace and magnitude of the cutting cycle.

The before strategy (pre-FOMC positioning): In the week before an FOMC meeting, the CME FedWatch Tool publishes real-time market-implied probabilities for each possible rate outcome based on federal funds futures prices. These probabilities represent the consensus expectation already priced into the market. A meeting where FedWatch shows 90% probability of a 25-basis-point cut is one where the cut is almost fully discounted. Any deviation from this consensus, whether the Fed cuts by 50 basis points (more dovish than expected, bearish for USD) or holds rates unchanged (more hawkish than expected, bullish for USD), will produce a larger market reaction than the expected outcome.

Pre-FOMC positioning is appropriate when a clear positioning imbalance exists. If the market is pricing in 75% probability of a hold but leading economic data (stronger-than-expected CPI, robust NFP) points toward a dovish Fed cut, a pre-announcement long on EUR/USD (anticipating USD weakness from a surprise cut) may be justified with tight risk management. Position size should be reduced to 50% of normal to account for binary outcome risk.

The after strategy (post-FOMC trend trading): The most reliable FOMC trading approach for retail traders is to wait for the decision, the statement, and at least the first 30 minutes of Chair Powell's press conference before entering any position. The press conference frequently causes additional volatility as the nuance of the Fed's thinking becomes clearer through questions and answers. Once the initial volatility settles and a directional trend emerges on the 15-minute or 1-hour chart, the post-FOMC trend trade is entered in that direction.

Post-FOMC trend trades that reflect genuine policy surprises or significant changes in forward guidance can generate directional moves of 100 to 300 pips over two to five days as the full implication of the Fed's communication is absorbed by the market. These multi-day trends are well-suited to swing trading on the 4-hour chart with wide stops that account for potential retracement before continuation.

Interest Rate Differentials and the Carry Trade Strategy Explained

The carry trade is a structured forex strategy that exploits interest rate differentials between currencies by simultaneously borrowing in a low-interest-rate currency and investing in a high-interest-rate currency, profiting from the difference in rates (the carry) in addition to any favorable exchange rate movement.

In 2026, the most prominent carry trade pairs reflect the significant interest rate differential between Japan and most other major economies. With the BOJ maintaining its policy rate at approximately 0.50% while the Fed holds at 4.25%, the RBA (Reserve Bank of Australia) at 4.10%, and the RBNZ (Reserve Zealand Reserve Bank) at 3.75%, the interest rate differential between JPY and AUD, NZD, and USD remains substantial.

A carry trade in AUD/JPY, for example, works as follows. The trader borrows Japanese yen at a low interest rate, converts to Australian dollars, and holds Australian dollar deposits or bonds at the higher Australian interest rate. The daily positive swap payment received for holding a long AUD/JPY position reflects this differential. At the current rate differential of approximately 3.60 percentage points between the RBA and BOJ rates, a $100,000 AUD/JPY long position generates approximately $9.86 per day in positive swap income ($3,600 per year), or roughly $1.30 per day for a $10,000 micro-lot position.

Recommended Articles

MARKET NEWS ANALYSIS

MARKET NEWS ANALYSIS

The carry trade has historically been profitable during extended periods of global economic stability and risk-on sentiment. Between 2003 and 2007, the yen carry trade generated enormous returns as global growth was strong, volatility was low, and JPY depreciated against high-yielding currencies. It became violently unprofitable in 2008 when the global financial crisis caused risk-off conditions and a sharp JPY appreciation as yen was repatriated.

In 2026, the carry trade in JPY pairs remains viable but requires active monitoring of BOJ policy developments. The BOJ's gradual normalization of its ultra-accommodative policy, which began with the abolition of yield curve control in 2024 and continued with cautious rate increases in 2025, creates periodic risk of sudden carry trade unwinds when markets interpret BOJ statements as more hawkish than expected. These unwinds can produce rapid JPY appreciation of 200 to 500 pips in hours, requiring carry trade positions to be managed with clearly defined stop losses rather than held passively with no risk management.

ECB, BOE, BOJ, and RBA: How Each Central Bank Moves Its Currency in 2026

Understanding the individual characteristics and current policy stance of each major central bank allows traders to anticipate which communication events and data releases will drive the most significant currency moves for each pair.

European Central Bank (ECB): The ECB manages monetary policy for the 20 eurozone member states. In 2026, the ECB is navigating a delicate balance between supporting economic growth in Germany and France (which have shown weakness in recent quarters) and managing persistent services inflation across southern European economies. ECB President Christine Lagarde's press conferences following each rate decision are frequently the primary EUR driver of the week, as the nuance of the bank's communication about future rate direction often diverges from simple rate decision outcomes. EUR/USD is most sensitive to the divergence between ECB and Fed policy expectations. When markets expect the Fed to cut more aggressively than the ECB, EUR/USD tends to rise. When the ECB is expected to ease more aggressively, EUR/USD falls.

Bank of England (BOE): The BOE's Monetary Policy Committee (MPC) meets eight times per year and publishes a Monetary Policy Report quarterly that includes updated economic projections. UK-specific inflation dynamics (persistent food and energy price pressures in 2025 and 2026), the ongoing adjustment to post-Brexit trade patterns, and a domestic housing market sensitive to mortgage rate changes all make BOE policy particularly complex to forecast. GBP/USD (Cable) is the most sensitive major pair to BOE decisions. BOE meetings where the MPC vote is split (some members voting for cuts while others vote for holds) produce significant intraday GBP volatility as the composition of the vote is revealed.

Bank of Japan (BOJ): The BOJ remains the most unique major central bank in 2026. After decades of near-zero or negative interest rates and an explicit yield curve control policy, the BOJ began a cautious normalization process in 2024. In 2026, every BOJ meeting carries the potential for policy surprises that can produce 100 to 300-pip JPY movements within hours. The BOJ's communication has historically been less transparent than Western central banks, making Governor Ueda's press conferences particularly impactful as the primary source of policy guidance. Long USD/JPY positions in 2026 require consistent monitoring of BOJ headlines given the binary risk of sudden yen-strengthening events.

Reserve Bank of Australia (RBA): The RBA meets eleven times per year and its decisions primarily affect AUD pairs. In 2026, the RBA's policy path has been influenced by domestic inflation in services and housing, Chinese economic demand for Australian commodity exports, and the broader Asia-Pacific economic cycle. AUD/USD is additionally influenced by iron ore and copper prices, making it a dual-driver pair where both RBA policy and commodity market conditions must be monitored. When Chinese industrial data is strong and iron ore prices are rising, AUD benefits from both commodity and trade flow channels simultaneously.

Building a Macro Fundamental Bias for Directional Forex Trading

A macro fundamental bias is a directional view on one or more currency pairs based on the relative monetary policy stance of the two central banks involved, combined with relative economic strength assessments.

The process for building a weekly macro bias takes approximately 45 minutes on Sunday evening and produces a directional framework that informs all trading decisions for the week.

Step one involves reviewing the current interest rate differential for each monitored pair. Which central bank in the pair has the higher rate? Which direction is each bank currently moving rates? A pair where one central bank is hiking while the other is cutting has the maximum policy divergence and therefore the strongest structural fundamental trend.

Step two involves reviewing the most recent central bank meeting minutes and any speeches made by central bank officials since the last meeting. These communications often contain the clearest forward guidance about the next policy decision and can shift market expectations meaningfully.

Step three involves identifying which high-impact economic releases are scheduled for the coming week that could alter the current policy expectations for either central bank in the monitored pairs. An unexpected CPI reading or NFP miss can shift policy expectations enough to produce a multi-day fundamental-driven currency move.

Step four involves expressing the bias as a directional statement: for example, the bias for EUR/USD this week is bearish because the Fed is expected to hold rates higher for longer relative to the ECB, the dollar is supported by strong recent US labor market data, and no data releases this week are likely to significantly alter this divergence. This bias then acts as the directional filter for all technical trade setups taken during the week. Technical setups aligned with the macro bias are given full position sizing. Counter-bias setups are either skipped or traded at half size.

Key Takeaways on Interest Rates and Forex in 2026

Interest rate differentials between central banks are the most powerful and persistent fundamental driver of currency pair direction. The Federal Reserve, ECB, BOE, and BOJ each have distinct communication styles, policy frameworks, and domestic economic pressures that create different opportunity profiles for the pairs they influence. The carry trade exploits interest rate differentials systematically but requires active risk management to survive periodic unwind events. Building a weekly macro fundamental bias through central bank communication review, interest rate differential assessment, and scheduled data event analysis provides the directional context that elevates technical trading from reactive chart-reading to proactive, high-conviction directional positioning.

Financial Disclaimer: This content is for educational purposes only and does not constitute financial advice. Forex trading involves significant risk of loss. Interest rate analysis does not guarantee future currency direction. Always seek independent financial guidance before trading.